In Evans v Barclays Bank and others the UK Supreme Court allowed the banks’ appeal and reinstated the specialist tribunal’s refusal to certify Phillip Gywn James Evans’ application for opt-out collective proceedings in a follow-on foreign exchange (FX) damages claim, emphasising the breadth of the Tribunal’s discretionary case-management role and the limited proper scope of appellate intervention.

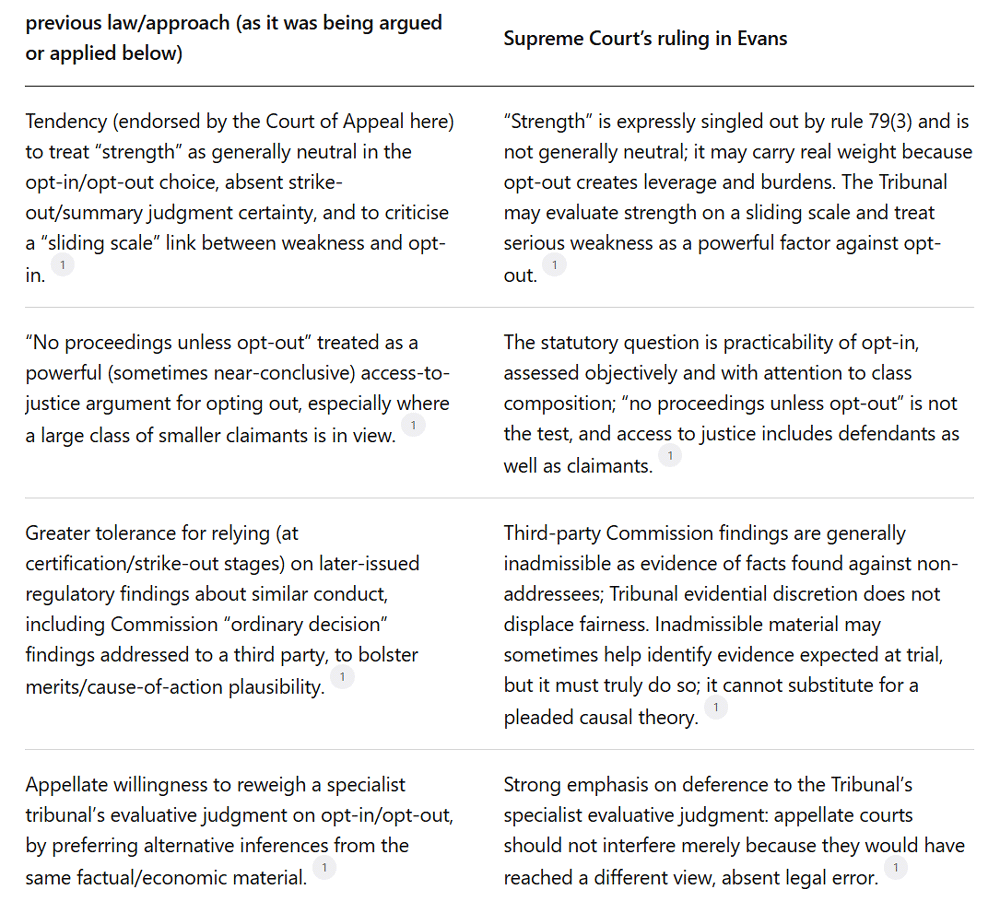

For solicitors, the practical message is that the opt-in versus opt-out choice under rule 79(3) is a structured balancing exercise in which (i) the “strength of the claim” can carry real, case-dispositive weight on a sliding scale (even where strike-out is not yet ordered) and (ii) “practicability” is assessed objectively, with careful attention to class composition (including whether a meaningful core of sophisticated claimants could realistically run opt-in claims).

The court also delivers an important evidential holding: factual findings in a European Commission “ordinary decision” addressed to a third party (here, Credit Suisse) are not admissible as evidence of the facts found against non-addressees in the Tribunal, and do not gain traction merely because proceedings are at an interlocutory stage. This narrows a route some claimants had begun to use to bolster weak causation theories at certification/strike-out stages.

Background and procedural history

The judgment is one of the court’s most consequential interventions since the 2015 reforms to collective competition litigation: it concerns how the Competition Appeal Tribunal should decide whether certified collective proceedings proceed on an opt-in or opt-out basis, given the “powerful” leverage and cost risks of opt-out class actions and the Tribunal’s gatekeeper role.

Procedurally, this is a follow-on damages claim relying on European Commission FX settlement decisions, with the litigation unfolding over several years: an application to bring opt-out collective proceedings was filed in late 2019; certification hearings took place in July 2021; the Tribunal handed down its judgment in March 2022; further Commission decisions were published in July 2022 (after the Tribunal’s decision); the Court of Appeal allowed the appeal in November 2023; and the Supreme Court heard the appeal in April 2025 and handed down judgment in December 2025.

The decision also sits within a cluster of linked appeals concerning the same proposed collective action against multiple banks. For present purposes, the case page for UKSC/2023/0173 records the appellants in that appeal as NatWest Markets plc and NatWest Group plc, and shows the judgment was delivered on 18 December 2025 under neutral citation [2025] UKSC 48.

Facts and pleaded theory of harm

At a high level, the case arises from European Commission findings (in settlement decisions) that certain FX traders employed by major banks exchanged commercially sensitive information in private chatrooms and occasionally coordinated aspects of FX spot trading. The infringements were characterised as “by object” and (as settlement decisions) did not involve a full assessment of actual market effects, which matters because loss and causation still have to be proved for damages claims.

Mr Evans’ pleaded theory sought to convert those infringement findings into a very wide damages claim. He proposed two claimant classes: one class defined by transacting directly with the defendant banks during relevant participation periods, and a second class based on an “umbrella effect” theory extending alleged harm to trades with other financial institutions during the infringement period. The claim alleged persistent, market-wide widening of bid-ask spreads across a very large volume of trading, supported by expert evidence and an aggregate damages approach, with class sizes in the tens of thousands and an indicative aggregate damages figure in the billions.

The Tribunal’s underlying concern (later central to the Supreme Court’s reasoning) was the pleaded gap between the Commission’s bounded findings (limited traders, limited communications, and limited temporal commercial value) and the breadth of the pleaded causal mechanism and class definitions. That gap informed both the Tribunal’s strike-out concerns and its refusal to permit the proceedings to continue on an opt-out basis.

The Supreme Court’s decision and clarified tests

The legal framework is rule 79(3) of the Tribunal Rules, operating alongside the Tribunal’s overriding objective (just disposal at proportionate cost) and the statutory architecture for collective proceedings under the Competition Act 1998. Rule 79(3) expressly identifies two focal factors for the opt-in/opt-out choice: “strength of the claims” and whether it is “practicable” to bring proceedings as opt-in collective proceedings, in the context of a broad discretion to take account of all relevant matters.

The Supreme Court framed four issues:

- whether the Court of Appeal had been wrong to treat “strength” as generally neutral;

- whether it had been wrong on “practicability”;

- whether it had over-weighted broad policy ideas (vindication of rights/deterrence) in favour of opt-out; and

- whether it had been wrong to treat a post-dated Commission ordinary decision addressed to a third party as admissible and probative.

On “strength”, the court rejects the idea that merits are normally neutral at the opt-in/opt-out stage. Instead, it links strength to procedural fairness and proportionality: opt-out procedure creates settlement pressure (“leverage”), administrative burdens and litigation cost exposure for defendants, and therefore requires greater justification as merits weaken; conversely, confidence in a strong claim can justify deploying opt-out’s heavier machinery. The court’s own summary captures the direction of travel: strength is not all-or-nothing, and is properly evaluated on a sliding scale.

The court also ties this to disciplined pleading and evidential realism. In a follow-on claim based on “by object” settlement decisions, infringement is established but causation and loss mechanisms remain to be pleaded and ultimately proved. The Tribunal was therefore entitled to expect a properly articulated causal bridge between the infringement and the scale of loss claimed, rather than reliance on speculative hopes that large-scale disclosure might generate a workable case later.

The judgment’s most citeable distillation of this point is deliberately practical:

“if the claim is very weak it is likely to be more difficult to justify resort to the opt-out procedure” (para 94).

On “practicability”, the court emphasises an objective assessment rather than a subjective inquiry into whether this particular market cohort will, in fact, opt in—partly because evidencing subjective reasons risks privilege complications and is often infeasible at scale. The Tribunal should examine class composition, identify distinct groups with different profiles and claim sizes where appropriate, assess opt-in practicability for each group, and then “stand back” for an overall balance of justice.

Applied to the facts, the court accepted that the Tribunal was entitled to conclude that opt-in claims were practicable overall where a significant, sophisticated group (with meaningful individual claim value) could reasonably be expected to litigate on an opt-in basis, even if a larger tail of individuals/small entities would struggle to do so—and even if, in practice, some of the sophisticated cohort did not wish to engage. It follows that “no claim unless opt-out” is not the statutory test; the statutory focus is practicability, not inevitability.

On broader policy arguments, the court holds that vindication and deterrence are aims of the collective proceedings regime but are not free-standing reasons to favour opt-out over opt-in; they must be balanced against the countervailing policy of protecting defendants from oppressive or inflated litigation. The governing starting point is even-handedness: “without any presumption or predisposition” (para 168).

On the evidential point, the Supreme Court holds that the common law rule associated with Hollington v Hewthorn applies in the Tribunal: findings of fact by another decision-maker are generally inadmissible as evidence of the facts found, because the fact-finding tribunal must evaluate evidence for itself as a matter of fairness, especially where the party against whom the findings are deployed was not a party to the earlier process. The Tribunal’s procedural discretion over evidence does not displace that fairness principle.

The court accepts that material inadmissible at trial can sometimes assist at interlocutory stages by identifying evidence reasonably expected to be available at trial (for example, where a prior decision records underlying evidence rather than simply expressing evaluative findings). But it considered the Commission ordinary decision relied on by the Court of Appeal did not, in substance, provide the missing link in this case: it was addressed to a third party, concerned a different infringement, and did not properly supply probative findings capable of supporting causation in the pleaded claims against these defendants.

The result is straightforward: the Supreme Court allows the appeal and reinstates the Tribunal’s refusal to certify opt-out proceedings.

Practical implications for solicitors

For claimant-side solicitors, Evans increases the premium on front-loaded pleading and evidential architecture. A follow-on infringement finding (particularly a by-object settlement decision) is not a shortcut around the hard work of causation: “infringement happened” does not itself answer “this class suffered this loss in this way at this scale”. The judgment signals that the Tribunal may regard gaps in causation pleading as a major reason to refuse opt-out certification, and that a claimant cannot justify compelling vast disclosure simply in the hope that something helpful will turn up.

For defendants, Evans is both a shield and a playbook. It supports targeted resistance to opt-out certification by (i) isolating weaknesses in the pleaded causal mechanism and mismatch between infringement findings and alleged market-wide loss, and (ii) building a practicability narrative that focuses on who the real economic beneficiaries are and whether a meaningful core of sophisticated claimants could pursue opt-in claims. It also enables early evidential objections to attempts to rely on third-party regulatory findings as de facto proof of facts.

For transactional solicitors advising corporates and financial institutions, Evans affects how competition exposure is diligenced and allocated. It does not eliminate opt-out collective proceedings risk, but it suggests (at least in some market settings) that defendants can resist opt-out orders where the claim theory is weak or where the class includes substantial sophisticated players who could litigate opt-in. That should feed into how you assess real-world probability of an opt-out class action being allowed to proceed (distinct from the quantum that might be claimed).

Recommended steps for solicitors

The following practice points translate Evans into workstreams (pleadings, evidence, privilege, funding and risk allocation) that solicitors can implement immediately.

Litigation checklist (claimant-side)

- Map the infringement findings to the pleaded class definitions and to a causation narrative that is not dependent on speculative future disclosure; ensure the pleaded causal chain explains scope (who), time (when), mechanism (how), and market coverage (how wide).

- Treat rule 79(3)(a) as potentially determinative: prepare for the Tribunal forming a high-level merits view that can weigh heavily against opt-out if the claim is weak.

- Build a practicability record that deals with class composition granularly (not just averages): if the class includes sophisticated high-value claimants, consider whether the proposed class can realistically be carved differently (or whether opt-in is strategically unavoidable).

- Plan funding on the assumption that “opt-out as last resort” arguments will not carry the day; consider whether a viable opt-in model exists for the likely core claimant group.

- Be cautious in deploying third-party decisions: they cannot substitute for evidence or pleaded causation, and may be excluded as inadmissible findings rather than admissible evidence.

Litigation checklist (defendant-side)

Make “mismatch” central: contrast the limited nature of infringement findings (scope/participants/timing) with the breadth of pleaded loss theories and class definitions.

Resist disclosure-driven pleading: emphasise that compelling massive disclosure is not justified where the causal mechanism is not plausibly articulated.

Frame practicability as an objective inquiry: show how a reasonable sophisticated claimant with meaningful potential recovery could bring opt-in claims, and highlight where the aggregate value of small-claim cohorts is tiny relative to the total.

Use evidential admissibility proactively: object to reliance on third-party findings as proof, distinguishing between admissible recorded evidence and inadmissible evaluative findings.

In appeals, anchor submissions in deference to specialist evaluative judgment and the absence of error of law; Evans materially strengthens that line.

Transactional practice points

When diligencing a target with historic competition investigations/decisions, analyse not only infringement risk but also (i) plausibility of downstream causation theories and (ii) likely claimant-class composition (consumer-small-claim vs sophisticated-high-value mix), because that mix now matters more at the opt-in/opt-out gateway.

Consider drafting risk allocation (warranties/indemnities, disclosure schedules, litigation conduct clauses) with a clearer distinction between opt-in follow-on exposure (fewer, larger claims) and opt-out exposure (mass claims with settlement leverage), reflecting the court’s emphasis on leverage and fairness.

Critique and what happens next

Evans has obvious strengths. It reinforces the coherence of the statutory design by tying opt-out certification to proportionality, fairness and the Tribunal’s overriding objective, rather than treating opt-out as a near-automatic access-to-justice mechanism whenever a large class exists. It also enhances legal certainty by clarifying that rule 79(3)’s express reference to “strength” matters, and by providing a principled evidential rule that prevents third-party regulatory findings from being weaponised as quasi-proof against defendants who could not participate in the earlier process.

There are, however, plausible weaknesses and pressure points. First, the more weight “strength” carries at the opt-in/opt-out stage, the more the certification process risks becoming resource-intensive (and, in practice, closer to merits argument) even though the Tribunal is not conducting a trial. That cuts both ways: it can screen out weak claims early, but it may increase front-loaded costs and procedural heat in complex cases where merits and economic evidence are genuinely hard to assess early.

Secondly, the court’s objective approach to practicability is conceptually clean but may sit uneasily with market realities. A scheme that is “practicable” in the abstract may still not attract opt-in participation in the real world (for reasons ranging from commercial relationships to cost/benefit perceptions). Evans makes clear that “no proceedings unless opt-out” is not the governing test, meaning some categories of low-value claimant may remain practically unremedied unless a fundable opt-out structure exists – raising familiar policy debates about under-enforcement versus over-enforcement in private competition damages.

Looking ahead, two litigation trends are likely. First, we should expect more aggressive use of strike-out/summary judgment mechanisms in and around certification hearings, especially where defendants can characterise the pleaded causation theory as speculative or structurally mismatched to infringement findings. Secondly, evidential skirmishing about what can properly be deployed at interlocutory stages – particularly where regulatory material records “evidence” versus “findings” – is likely to intensify, with Evans providing the vocabulary and constraints for those arguments. Any legislative response is less predictable, but Evans equips Parliament and policy-makers with a clearer articulation of the court’s concern about settlement leverage and disproportionate burdens as reasons to keep opt-out certification tightly controlled.

Cite this work:

To cite this resource, please use the following reference:

National Case Law Archive, 'Evans: Supreme Court tightens the route to opt-out competition collective proceedings' (LawCases.net, February 2026) <https://www.lawcases.net/analysis/evans-supreme-court-tightens-the-route-to-opt-out-competition-collective-proceedings/> accessed 27 July 2026

Articles and content on this site are for informational purposes only and do not constitute legal advice. Do not rely solely on this information.